It has now passed two years since the beginning of what has become known as the Red Sea Crisis. After Yemen’s Houthi militants started targeting cargo vessels in the waterways around the Suez Canal in late November 2023, most of the major containership operators moved to divert their sailings around Africa. This adds distance, time, and cost to your shipments.

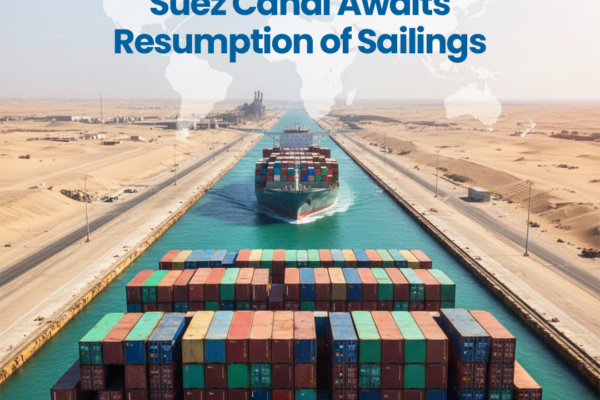

This sea passage through the Red Sea has traditionally accounted for around 12% of global trade, including several million tonnes of cargo to and from Australia annually. The number of container ships transiting Suez Canal in November 2025 was 120, down from 583 in October 2023, shortly before the escalation of Houthi attacks.

Some container lines are tentatively starting to use the Suez Canal again. Last week, CMA CGM announced that from 15 January 2026, its Indamex service between India/Pakistan and the U.S. east coast would transit the Suez in both directions, as part of a scheduled operation.

Other major players like Maersk and Hapag-Lloyd, however, are waiting for more sustained safety and stability, emphasising that crew and vessel safety remain paramount, with a view to a very gradual return to the route. Those two carriers formed the Gemini network earlier this year—a collaboration designed to cut their costs and improve schedule reliability.

An unintended beneficiary of the Red Sea Crisis has been the air cargo industry, which has seen a marked increase in demand from Asia to the Middle East and Europe since 2024. When sea carriers return to the route, goods carried temporarily by airfreight are likely to shift back to ocean shipping, hitting growth expectations.

The news for air cargo is not all bad though. While demand from China to the U.S. may have fallen due to uncertainty surrounding the U.S. tariff strategy, demand has shifted to Europe, Southeast Asia, and the Middle East.

Airfreight figures for the middle of 2025 show that traffic from China to the U.S. declined by 29% year on year, while demand from China to Europe increased by 35%, and from China to ‘Other’ Asia Pacific destinations improved by 25%. Vietnam seems to be at the forefront of rapid airfreight growth in the Asian region.

It will be interesting to get updated figures for sea cargo in 2026 to see if the trend likewise drops from China to the U.S., and flows back more towards the Middle East and Europe. We do know that there has already been an increase in container shipments among Asian countries themselves—rather than to the U.S.—during the course of 2025.

A return to Suez by the major containership lines will reduce transit times, and could possibly also flood the market with released capacity—due to ships being freed from Africa routes—putting downward pressure on freight rates.

A sudden surge of vessels to a full-scale, simultaneous return is unlikely soon, as carriers balance shorter routes with potential overcapacity and port congestion. We expect to see a controlled shift over a timeframe of 60-90 days—hopefully in early 2026—once the major carriers consider conditions to be truly safe and stable.

Here at Colless Young, we keep up to date on all shipping trends, including movements at critical ‘chokepoints’ such as the Suez Canal. Talk to us about the effects that changes to shipping routes might have on your transit times and freight rates.